Settling chain transactions: accountants’ check-list

August 3, 2020

What are chain transactions?

As the world economy becomes more integrated, the volume of international trade increases each year. It is not uncommon to see companies focus their activities on importing goods from afar for sale in their region. This is an example of a ‘chain transaction’, in which at least two sale transactions occur between at least three business operators. What is characteristic for chain transactions is that each of the transactions within a chain is regarded as a sale, yet only one transport happens. As accountants, we might not be aware of being involved in a chain transaction, especially when we are its final link. Yet, from a legal perspective, it is our duty to verify, whether we are a link in a supply chain transaction. This article is a four-step guide on how we should approach settling chain transactions.

1 – Identify all parties involved in the chain transaction

It is crucial to establish whether we are involved in a chain of supply, especially when in a position of being the final buyer. This will influence if we are to settle our acquisition as an import or as a domestic supply. We can verify this through a brief look at the CMR (International Consignment Note), which should name all parties involved in a transaction. Alternatively, we can inquire with our supplier to ask whether they take responsibility for organising the transport of goods.

2 – Identify the party in charge of shipping:

If we are indeed dealing with a chain transaction, our next step is to identify the party arranging shipment. This is important for assessing which supply is to be viewed as the ‘moveable’ supply – the transaction linked to the transport of goods. Determining the moveable supply allows us to assess, which of the supplies is to be settled as intra-community chain transaction/export of goods – as there can only be one of these per chain. All other transactions are to be settled as domestic supply. This is particularly important for moveable supplies between EU Member States, as such transactions are qualified for a 0% VAT rate.

3 – Determining the moveable supply

To do so, we ought to identify the countries, in which the business operators involved in a supply chain are based. This will help with establishing, which countries are involved in the intra-community supply of goods (ICS) and intra-community acquisition of goods (ICA). ICS will always be linked to the country in which shipping begins, ICA – with its destination. All transactions occurring before the moveable supply are taxable in country of origin (under local tax codes), all transactions following it – in country of destination (also following local tax codes). We settle moveable transactions at country of destination, i.e. a supply of goods from a French manufacturer to a Polish buyer, facilitated by a German middleman, is to be settled in Poland, following Polish tax laws.

4 – Determining terms and conditions of supply: INCOTERMS2020

If a middleman company is in change of arranging transportation, it is crucial for us to determine the exact moment, in which economic ownership passes over from the supplier to the acquisitor. At that moment, the legal right manage and dispose of goods acquired is transferred over to the buyer. With it, the risks regarding transportation and storage are transferred as well. The moment of change of economic ownership is also when the buyer becomes liable for tax on an acquisition.

In most cases, change of ownership is determined by the agreed upon rules of change of ownership, designated with a corresponding INCOTERM code, updated approx. every 10 years. The table below lists the most commonly used INCOTERMS2020. From an accountant’s perspective, change of ownership as dictated by INCOTERMS influences when we are to settle the transaction. Ex.: we sell goods to a contractor in late June, and send the goods for shipping by the end of the month. Under the DAP INCOTERM, the transaction will come to be liable for taxation and to be settled in July, once the shipment reaches our contractor.

| INCOTERM2020 | CHANGE OF ECONOMIC OWNERSHIP | |

| CODE | FULL NAME | |

| EDW | EX Works | When goods have been made available for transport outside supplier's warehouse |

| FCA | Free Carrier | When goods have been loaded onto a vehicle |

| CPT | Carriage Paid To | When goods have been handed over by the buyer to the carrier |

| CIP | Carriage and Insurance Paid To | When goods have been handed over by the buyer to the carrier |

| FAS | Free Alongside Ship | When goods have been placed by a maritime vessel |

| FOB | Free on Board | When goods have been loaded onto a maritime vessel |

| CIF | Cost, Insurance, and Freight | When goods have loaded onto a maritime vessel |

| CFR | Cost and Freight | When goods have loaded onto a maritime vessel |

| DAP | Delivered at Place | When goods are ready to be unloaded at buyer's warehouse |

| DPU | Delivered at Place Unloaded | When goods have been unloaded and handed over to the buyer |

| DDP | Delivered Duty Paid | When goods have been delivered to a place designated by the buyer |

Settling supply transactions

After all parties participating in a chain transaction, the party coordinating shipment of goods, and terms and conditions of shipment have all been identified, we can begin to settle the transition. The moveable supply is to be treated as export/import, with the party responsible for custom duty depending on INCOTERMS. Ex.: when following the EXW, it is the buyer who bears the costs of custom duty, following the DAP – it is the supplier. In a situation where both parties involved in a moveable supply are EU Member States, then the transaction is classified as intra-community supply/acquisition of goods (ICS/ICS), and is exempt from VAT. Remaining transactions are settled as domestic supplies. All transactions proceeding the moveable supply are settled in the country of origin, all following it – in the country of destination.

Accountants’ check-list

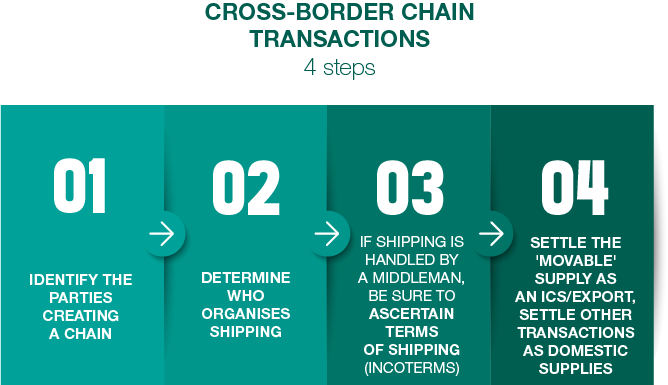

As international economic cooperation in steadily increasing, accountants encounter cross-border transactions more and more often. Cross-border chain transactions are a subset of these, where despite a long chain of transactions, only one shipment of goods takes place. When settling such a transaction, accountants should proceed as follows:

- Identify all parties involved in a supply chain

- Identify the party arranging the transport of goods

- Determine which supply in the chain is the ‘moveable’ supply

- Determine the terms and conditions of supply (the INCOTERMS)

These steps are necessary for settling cross-border chain transactions correctly for two main reasons. First, intra-EU moveable supplies are tax exempt, which is why it is crucial to separate them from unmoveable supplies – other transactions within a supply chain. Second, the INCOTERMS influence which party is to bear the costs associated with custom duty when the moveable transaction goes beyond the EU. INCOTERMS dictate when economic ownership of goods passes to the buyer, thus indicating when the transaction is to be settled.

Tags chain transactions, change of economic ownership, cross-border chain transactions, INCOTERMS2020, supply chain transaction, terms and conditions of supply